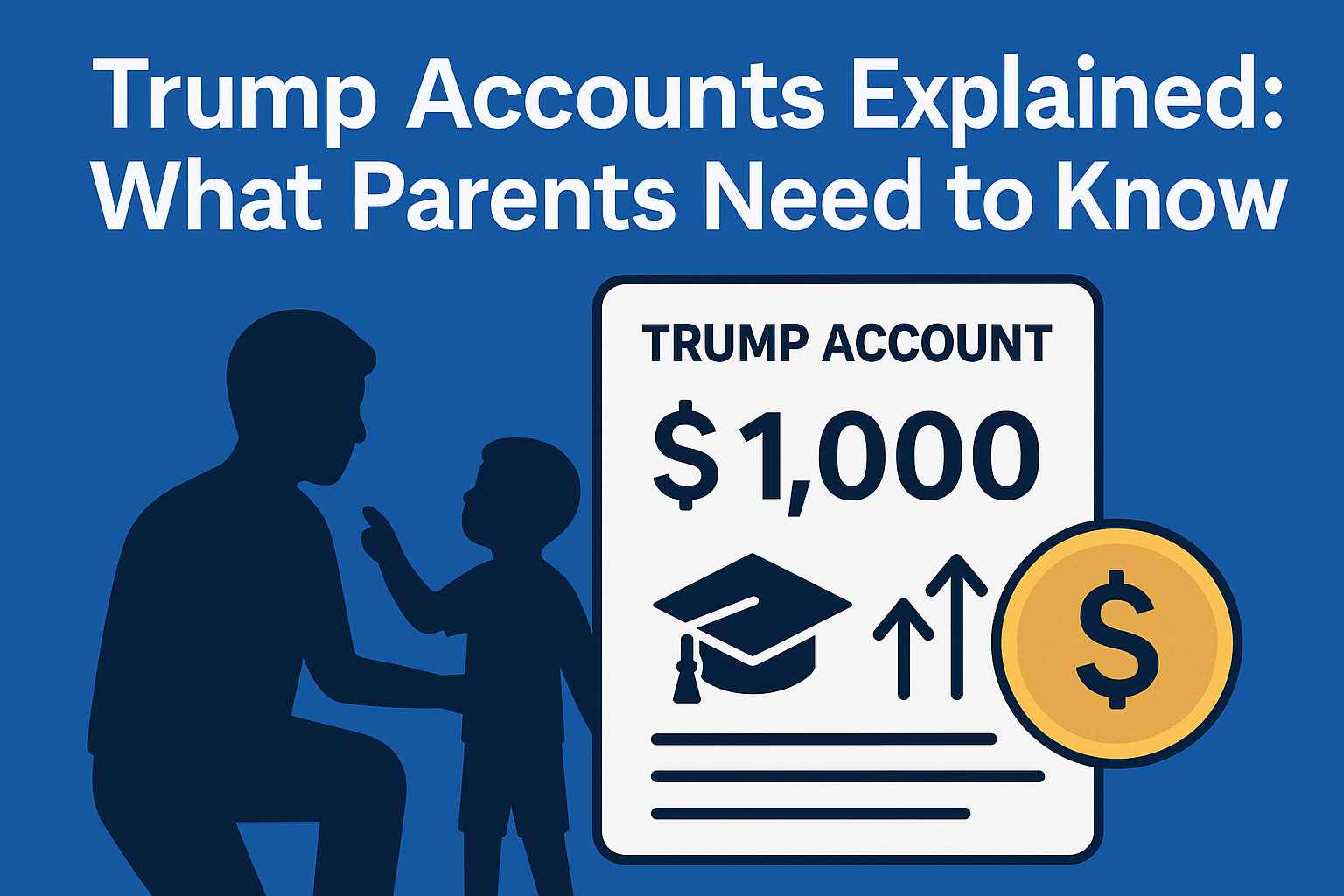

Trump Accounts are a new U.S. government–backed savings and investment program designed to give every child a financial head-start for the future. Launched under the One Big Beautiful Bill Act (2025), the scheme aims to build early wealth for millions of American children through long-term investing.

Below is a straightforward guide for parents.

🔹 What Exactly Is a Trump Account?

A Trump Account is a government-supported investment account for children under 18.

Money placed in the account is invested in broad U.S. stock-market index funds, allowing it to grow over time.

It works somewhat like a child-focused savings + investment plan — but with government funding and long-term growth potential.

🔹 Who Can Get a Trump Account?

Any child under 18 with a valid Social Security number is eligible.

Two groups benefit:

1️⃣ Children born between 2025–2028

They automatically receive a $1,000 government deposit when their account is created.

2️⃣ Children born before 2025

They can also open an account, but won’t receive the $1,000 seed.

This second group is exactly where the Dell family’s $6.25B pledge is targeted.

🔹 How Much Money Can Go Into the Account?

Up to $5,000 per year per child

Anyone can contribute: parents, relatives, employers, nonprofits

Employers can contribute up to $2,500 of that yearly limit

There is no limit on how many years a child can receive contributions — as long as the annual maximum is respected.

🔹 How Does the Money Grow?

All money in the account is invested in low-cost U.S. stock market index funds.

This allows the funds to grow over the years through:

Stock-market gains

Compounding returns

Regular yearly contributions

Because withdrawals are not allowed until age 18, the money remains invested long enough to potentially grow to a significant amount.

🔹 When Can Children Use the Money?

Funds can be withdrawn once the child turns 18 years old.

Unlike traditional education savings accounts, this money can be used for multiple major life goals:

✔ Education and college

✔ Buying a first home

✔ Starting a business or startup

✔ Further investing

✔ Other long-term needs

This flexibility is one of the biggest advantages of Trump Accounts.

🔹 Why Were Trump Accounts Created?

The program aims to:

Give every child a financial foundation from birth

Reduce wealth gaps between low-income and high-income families

Encourage long-term investing habits

Build generational wealth through consistency and compounding

For many families — especially low- and middle-income households — these accounts may offer the first real chance at building meaningful savings for children.

🔹 How Do Parents Set Up a Trump Account?

Parents or guardians must submit a special IRS form:

Form 4547 — Trump Account Registration

This form activates the account and triggers any seed contributions (depending on the child’s birth year).

The full nationwide rollout begins on:

📅 July 4, 2026

From that date onward, families can set up accounts and start contributing.

🔹 What Does the Dell Pledge Mean for Families?

Michael and Susan Dell’s $6.25 billion donation will deposit $250 into Trump Accounts for 25 million children aged 10 and under — mainly those born before 2025 who don’t qualify for the government’s $1,000 seed.

This makes millions more children eligible for a meaningful financial start.

🔹 Bottom Line for Parents

Trump Accounts are designed to be simple, flexible and long-term:

They’re easy to open

They build wealth quietly over time

They can grow significantly by age 18

They support major life goals like education or homeownership

For many families, this program could become a powerful tool to support their child’s future.

Can Other Countries Follow the Trump Accounts Model?

Short answer: Yes, they can — but with major conditions.

The Trump Accounts model is essentially a Child Investment Savings Account backed by:

A government seed deposit

Optional private or employer contributions

Long-term stock-market investment

Access at adulthood for education, business, or homebuying

Many countries already have similar partial programs, but not at this scale.

🌍 Which countries have similar systems?

Several nations already use child-savings or investment accounts:

United Kingdom — Child Trust Fund (CTF)

Launched in 2005

Government deposited £250–£500 for every newborn

Funds grew tax-free until age 18

Very similar concept (but later discontinued due to costs)

Canada — RESP (with government grants)

Government adds matching funds

Money grows tax-free

Mainly for education

Singapore — Baby Bonus + CDA

Government contributes money into a child’s development account

Used for education, healthcare, childcare

Australia — Future Fund proposals

There were proposals for child investment funds using national wealth revenue

Not implemented at national level

South Korea — Child Development Accounts

Government supports savings for low-income children

Withdrawals allowed at adulthood for education/home

These models prove countries can follow a similar plan, but policies vary depending on budgets and goals.

💡 What a Country Needs to adopt the “Trump Account” System

1️⃣ Strong capital markets

Money must be invested safely in:

Index funds

Government bonds

National stock markets

Countries with unstable markets may struggle.

2️⃣ Government budget capacity

Seed money (like $1,000 per child) costs billions.

Only countries with:

Stable tax revenues

Budget surpluses

Strong economic growth

can afford it.

3️⃣ Financial literacy & digital systems

Parents must be able to:

Open accounts

Track funds

Make contributions

Withdraw safely

Need strong banking + digital identity systems.

4️⃣ Political support

These programs require:

Long-term planning

Multi-year budgets

Cross-party support

If governments change frequently, the scheme may collapse (as happened in the UK).

Yes, any country can adopt a Trump-Accounts-style program — but success depends on economic strength, political stability, and financial infrastructure.

It works best in countries that:

Have strong stock markets

Can afford large government seed deposits

Use digital systems for financial access

Want long-term wealth creation for citizens

Connect with us through social media

Facebook:

https://www.facebook.com/profile.php?id=61577015427068

https://www.facebook.com/profile.php?id=61577015427068X (Twitter):

https://x.com/tet_editor

https://x.com/tet_editorInstagram:

https://www.instagram.com/the_eastern_times_/?next=%2F&hl=en

https://www.instagram.com/the_eastern_times_/?next=%2F&hl=enMail (Email):

contact.theeasterntimes@gmail.com

contact.theeasterntimes@gmail.com