Money is important for a good life, but managing money is even more important for a balanced and stress-free life. You can earn millions, but if you don’t know how to manage it, your hard work and income will be wasted.

People are generally divided into three economic groups – poor, middle class, and rich. Without financial knowledge, the poor struggle to survive, and the middle class finds it hard to manage their expenses. On the other hand, the rich, who understand money management, can enjoy life without financial worries. Learning how to handle money wisely can help anyone improve their financial situation.

Step 1: Keep a Record of Your Finances

To manage your money wisely, track all your earnings, expenses, debts, savings, and investments. You don’t need to be an accountant—anyone can do this with a simple record-keeping system.

How to Organize Your Records:

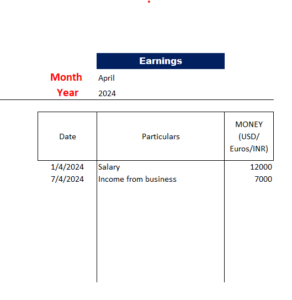

Monthly Earnings – Keep a dedicated page to record all sources of income.

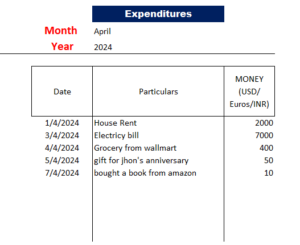

Monthly Expenses – List all your expenditures on a separate page.

Debts – Maintain a separate page to track any loans or money you owe.

Savings & Investments – Record your savings and investments on individual pages.

Emergency Fund – Keep a separate record for money set aside for emergencies.

At the end of each month, review your records. This will help you see where your money is going, how much you are saving, and identify unnecessary expenses. By analyzing your spending, you can make better financial decisions and improve your financial health.

Step 2: Create a Monthly Budget

After tracking your finances, the next step is to create a monthly budget for your expenses. This helps you control your spending and plan for savings and investments.

How to Plan Your Budget:

List all your expenses, including:

Household Expenses – Rent, electricity, water, internet, and other bills.

Daily Needs – Grocery, transportation, and medical expenses.

Financial Goals – Savings, investments, and emergency funds.

Personal Growth – Courses, books, and self-improvement activities.

Leisure & Fun – Entertainment, hobbies, and outings.

Budgeting for Different Lifestyles:

For Students – Plan for books, study materials, gifts for friends, extracurricular activities, entertainment, and savings.

For Families – Consider the needs of all family members, including education, healthcare, household expenses, and savings for the future.

By following a budget, you can manage your money wisely, avoid unnecessary spending, and work toward financial stability.

Step 3: How to Budget Your Monthly Expenses

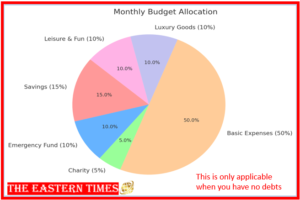

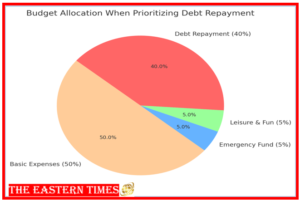

A well-planned budget ensures financial stability and helps you grow your wealth. Follow these simple budgeting rules to divide your income wisely:

Budgeting Guidelines:

- Savings (10-15%) – Save at least 10% of your income; if you earn more, aim for higher savings.

- Emergency Fund (5%) – Set aside 5% for unexpected expenses.

- Charity (5-10%) – Donate at least 5%, and if you earn more, consider giving more.

- Basic Expenses (50%) – Cover essential costs like rent, food, utilities, and transportation.

- Luxury Goods (10%) – Spend on valuable assets like gold, premium watches, branded clothing, or a car.

- Leisure & Fun (10%) – Enjoy entertainment, travel, and hobbies.

Step 4: Control Your Spending and Prioritize a Simple Lifestyle

To achieve financial stability, it’s important to control unnecessary spending and focus on a simple yet fulfilling lifestyle.

Ways to Reduce Unnecessary Expenses:

Avoid excessive shopping, unnecessary outings, and buying too many clothes.

Differentiate between needs and wants before making a purchase.

Reduce impulse buying and stick to a planned budget.

Embrace a Simple Lifestyle:

A simple life doesn’t mean lowering your standard of living—it means spending wisely.

Focus on quality over quantity when making purchases.

Remember, “Simplicity is the ultimate sophistication.”

By adopting a mindful approach to spending, you can reduce financial stress, save more, and enjoy long-term financial freedom.

Step 6: Build a Savings Fund and an Emergency Fund

Having both a savings fund and an emergency fund is essential for financial security and peace of mind.

1. Savings Fund

Set aside at least 10-15% of your income for future needs.

Use it for long-term goals like buying a house, education, or retirement.

Invest in secure options like fixed deposits, mutual funds, or retirement plans.

2. Emergency Fund

Save at least 5-10% of your income for unexpected expenses.

Helps in case of medical emergencies, job loss, or urgent repairs.

Keep it easily accessible in a separate bank account.

Having these funds ensures financial stability and prevents you from falling into debt during emergencies. Start small and build them gradually for a stress-free financial future.

Step 9: Keep a Credit Card for Emergency Backup

A credit card should only be used as a backup in financial emergencies, not for daily spending. Rely on your emergency fund first, but having a credit card ensures you don’t need to depend on others during crises. Use it wisely to avoid unnecessary debt and interest charges.

Step 10: Focus on Self-Improvement and Smart Living

Invest in self-improvement by reading books and gaining knowledge. Aim to own a house instead of renting. Start a kitchen garden to grow fruits and vegetables, reducing expenses. Prioritize exercise for physical and mental well-being, ensuring a healthier, more independent, and financially secure lifestyle.

Follow These Steps for 2 to 3 Months for Financial Stability

By consistently following these 10 steps for 2 to 3 months, you will notice positive results in your financial health. You’ll develop better spending habits, increased savings, reduced financial stress, and improved security. Stay disciplined, track your progress, and enjoy a stable and secure financial future.

Also read

https://theeasterntimes.com/how-to-manage-anxiety-and-stress-in-simple-ways/

ADVERTISEMENT